Factors Affecting Your Credit Score

Credit scores appear to be a hot topic lately. Especially with all these new mortgage rule changes, qualifying for a mortgage is definitely a contentious issue. Therefore, having a strong credit score will be important. With the desire to participate in the miles and points game, how do we juggle everything? Today, I will discuss all the factors affecting your credit score.

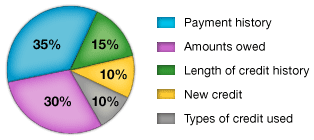

Payment history (35%)

Paying your bills IN FULL and ON TIME is the most important factor in your credit score. Bills include: car loan, cell phone on contract, credit cards, line of credit, personal loan, student loan and any other regular debts. Mortgage payments are actually not reflected on the credit report. Late payments or only paying partial or minimum balance will hurt your credit score.

Amounts owed (30%)

This is the credit utilization ratio. Where it measures the outstanding balance (when you statement closes) on your accounts in relation to the total credit available to you. Maintaining a low utilization ratio can improve your credit score. Ideally, you want to stay within the 1%-10% range. For example, if you have $10,000 in available credit, you will want to stay between $1 and $1,000 on your closing balances. Under 30% is also fair. Once you reach the 75% mark, it will start hurting your credit score. If you do not have a lot of credit limit, then try to pay your bills ahead of time, i.e. before the statement closing date, so that your closing balance won’t be so high.

Contrary to popular belief, this means that increasing your credit limit will help your score because it will reduce your credit utilization ratio.

Length of credit history (15%)

This factor is based on when the account was opened and the record of the last activity. The longer the history and the more activity, the larger the sample size to determine what kind of track record you have. Good or bad, most information will automatically be removed from your credit report after 6 or 7 years. You want to keep your credit report active by using your credit so that the credit bureau can get a clearer picture on how responsible you are with your available credit. If you have zero transactions and zero credit, you are not helping this factor.

New credit (10%)

Any time you open new credit, including a credit card, credit limit increase, a mortgage, etc., it will count as a credit inquiry and decrease your credit score generally between 5-30 points. The fear is that if you frequently apply for new credit, it can signal financial difficulty to the credit bureau. Furthermore, even time you check your credit score or credit report, you may be taking a hit. So all those free reports going on out there, not so free.

The contradiction is that if you do open more credit, it will help your credit utilization ratio if you do qualify for more credit.

Types of credit used (10%)

This factor accounts for the different kinds of accounts, such as credit cards, mortgages, retail loans, etc. The different types of credit gives an indication on how you manage your money. For example, loans with a deferred interest can indicate that you are unable to save up for a purchase. Consolidation loans can show that you have difficulty paying your debts. Manage your debts, by paying what is due on time will help this aspect.

Conclusion

As you can see, not one factor determine your entire credit score. Furthermore, some of these factors even contradict each other, which is why it is near impossible to have full score.

Hi Matthew, couple of quick questions.

a) Is credit utilization ratio calculated individually or cumulative? i.e. Can i go beyond 30% of credit limit on one card, but the overall utilization on all cards is under 30%, would this have an impact on the score?

b) “even time you check your credit score or credit report, you may be taking a hit. So all those free reports going on out there, not so free.” So frequent checks on creditkarma.ca might effect the score? hard vs soft enquiry?

It is calculated individually. They also factor in cumulative. That’s why it’s not a super straightforward calculation. Also if you have no activity on the other cards, it’s not moving your score one way or another. Should be a soft check for those free reports.

Matt,

Thanks for your comment on this. So If I received a card with a $3K and I need to hit minimum spending. If I put on this card let’s say $2k in the first month it will negatively affect my Credit Score. Even if I have another credit card with $20K limit and no use?

Keep in mind that it is not a perfect calculation, not so black and white. If you do put $2k on a card that has a $3k limit, I would pre-pay most of it before your statement closes.

thanks for clarifying I always paid in full but wait until the statement cames.

Hi, great blog!

The wife and I have been working at improving our creit scores for a few months now, signed up for a credit score monitoring service.

After several months of 5 points improvements on her score, the last month her score improved by 28 points, the big diference was her credit utilization went below 70%.

Cheers

That’s awesome. Thanks for sharing your experience!